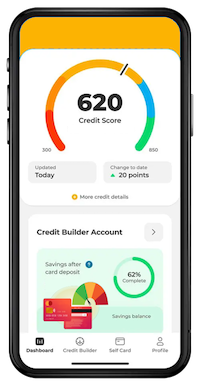

A credit score is a numerical value that reflects a person's creditworthiness, which is calculated based on their credit history. It is a measure of how likely an individual is to repay their debts on time, and is used by lenders, such as banks, credit card companies, and other financial institutions, to evaluate the risk of lending money to an individual.

A high credit score indicates that a person is a reliable borrower and is likely to repay their debts on time, making them more attractive to lenders. A low credit score, on the other hand, suggests that a person may be a risky borrower, which can make it more difficult to obtain credit or loans, and can result in higher interest rates and fees.

Having a good credit score is important because it can affect many aspects of a person's financial life, such as their ability to obtain a loan, get approved for a credit card, or even rent an apartment. A good credit score can also result in lower interest rates and better terms for loans and credit cards, which can save a person money over time.